engineering & technology publications

ISSN 1759-3433

PROCEEDINGS OF THE FIFTH INTERNATIONAL CONFERENCE ON ENGINEERING COMPUTATIONAL TECHNOLOGY

A Neural Based Model for Financial Credit Rating of Contractors

1Department of Construction Engineering, National Kinmen Institute of Technology, Taiwan

2Department of Construction Engineering, National Taiwan University of Science and Technology, Taiwan

In fact, the weight connection of the traditional BP is not optimum. The systemic characteristics of the background of information from a multiple-time-period or a multi-sourced training data can not be revealed. The internal noise of the training data also can not be filtered out. The problems mentioned-above cause a low percentage of correct BP output for credit rating. Therefore, this paper proposes the individual interactive adjusting learning rate model (IIALR) to promote the classification performance effectively. The IIALR model is built by the individual interactive adjusting learning rate (IIALR) technique and the batch-online weight updating frequency mode (BOWUF). Through the two new algorithms, the above-mentioned problems of traditional BP can be solved.

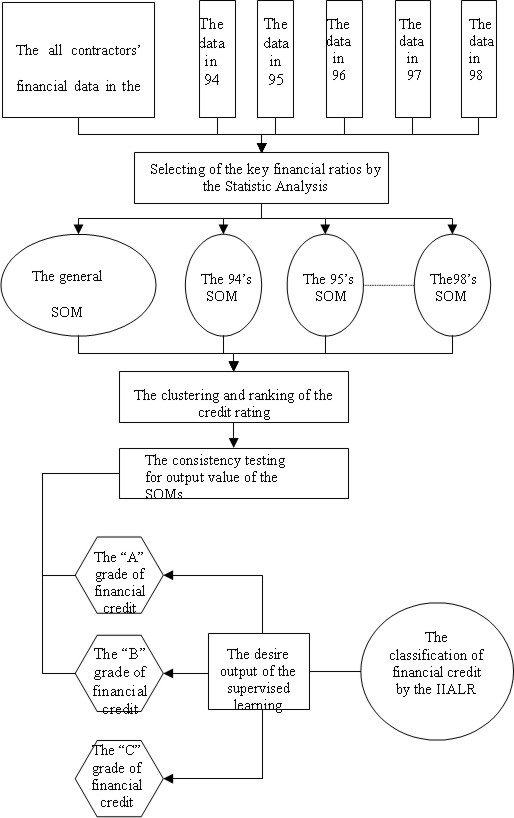

According to above-mentioned basic concepts of the credit rating model for contractors, this paper adopted the large scale contractors as the target of the case study. This paper adopts the following procedures to construct the model of credit rating for contractors. The procedure for constructing the model is shown in Figure 1. Moreover, to develop the simulation program of the model of contractors' credit rating for case study.

The model adopts Mann-Whitney-Wilcoxon testing to test the two data groups as a result of the normal distribution testing. The input vectors consist of the twelve key financial ratios. Through the clustering function of the SOM network, this paper used the key financial ratios as input variables of the model. Then, to rank every cluster of the contractor with no poor credit record from the SOM of the case study, this paper makes the entropy weight analysis for the characteristic vector of the sample of each cluster. It decides the grade of the financial credit for cases of each cluster, and the output of ranking of the clusters has passed the consistence testing.

The case study used the IIALR model for financial credit rating of contractors and showed that: the correct rate of the 89 training data is 97.31% and 90.91% for the 55 testing data sets. These results present an excellent performance of the credit rating model. This model also shows a better result when compared to the other models of using different algorithms.

Finally, this paper discusses the feasibility of applying the output of the model for the clients and contractors in practice and characteristics of the key financial ratios. For example, the key financial ratios, and the financial credit grade, can be used to describe the contractors' financial credit grades more effective, and also to provide important information for the contractors' prequalification and the contractors' financial management.

purchase the full-text of this paper (price £20)

go to the previous paper

go to the next paper

return to the table of contents

return to the book description

purchase this book (price £105 +P&P)